Financial Independence Faster When Nomading™

Ignoring Debt-To-Income

I am still preparing for the new series of classes and ultimately the new book by improving the charting engine for the Real Estate Financial Planner™ software.

It is tedious and slow going, but I’m making progress each day.

Today, while I was testing some of the charts, I came across this subtle one.

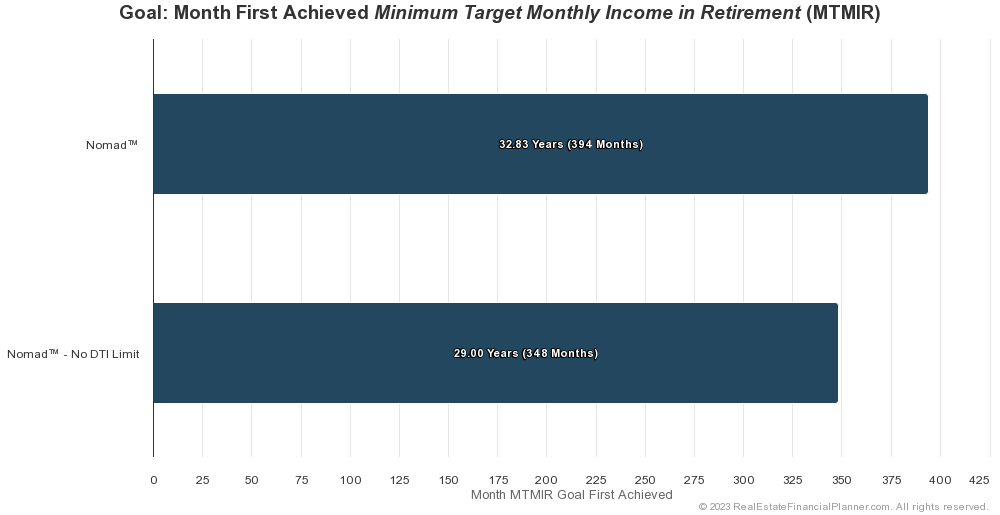

33 Years to FI

It shows that if this particular couple (John and Mary from the new classes/book) were to do the Nomad™ strategy with our current property price, interest rate and rent environment with saving a small amount of their income they’d be able to be financially independent in just under 33 years. This is Nomad™ in the chart above

SIDE NOTE: This is about 7 years faster than if they just invested in stocks and were able to get 10% per year in the stock market (which may be optimistic depending on your belief system and what they actually invest in). Often when modeling I assume 8% in the stock market to keep it conservative.

29 Years to FI

However, if they were able to buy properties without the 45% DTI ratio (or if they made more money and the 45% DTI was less of a factor) they’d be financially independent about 4 years faster. This is Nomad™ - No DTI Limit in the chart above.

They could do this by buying properties creatively (think subject to, owner financing, etc) or making more money to increase the income part of their debt-to-income calculation (side hustle, significantly higher income on their rentals from short-terms rentals or offering them on lease-options as a couple other examples).

Debt To Income

Have you ever read a book or taken a real estate investing course and wondered if you’d have enough income to qualify for all these loans? One way we look at that in the Real Estate Financial Planner™ software is by calculating debt-to-income for each month.

Here’s the debt-to-income chart showing how their debt-to-income looks for both traditional Nomad™ limited to never going above 45% debt-to-income ratio (which is what many lenders will want you to stay below with each new home purchase) and an ungoverned debt-to-income version of Nomading™ (the orange-colored Nomad™ - No DTI Limit in chart).

You’ll notice two significant spikes near the end… that’s when they achieve financial independence and therefore stop working. Their income drops considerably at that point spiking their debt-to-income ratio.

Love,

James Orr

The Real Estate Financial Planner™

P.S. This is a trivial example of the type of unprecedented insight I’ll be covering in the class and book… insight into how it actually looks to implement various real estate investing strategies.

Keep reading with a 7-day free trial

Subscribe to Real Estate Financial Planner™ to keep reading this post and get 7 days of free access to the full post archives.